Handing over the keys feels like the final step, yet your duties as a seller do not always stop at completion. Many homeowners assume that once contracts are exchanged and the money clears, every future problem becomes the buyer’s concern.

That assumption can prove expensive. A buyer typically has up to six years to bring a claim if something you said, or failed to say, turns out to be untrue. Getting to grips with seller liability after selling house UK is the smartest way to shield yourself from a stressful, costly dispute later on. This guide explains how long your responsibility lasts and how to stay in the clear.

Key Takeaways

- Sellers can usually face a claim for around six years once the sale completes.

- Deliberately hiding a known fault can extend that window, with the clock starting from discovery.

- Most claims stem from misrepresentation, misdescription, or hidden defects that existed before the sale.

- Honest answers on the TA6 disclosure form are your strongest protection against a future claim.

- Indemnity insurance helps with missing paperwork but never covers deliberate dishonesty.

Can You Be Held Liable After Selling a House?

Yes, you can. A seller in England and Wales may answer for problems for roughly six years after completion, and longer where a fault was deliberately hidden. Liability turns on what you declared during the sale and on defects that already existed before the handover.

Completion transfers ownership, but it does not erase the statements you made along the way. Your replies on the disclosure form and to your buyer’s enquiries travel with you. If one of those answers was wrong and the purchaser acted on it, a claim can land on your doormat months, or even years, later.

| The reassuring part: genuine honesty throughout the sale removes almost all of this risk. |

How Long Does Seller Liability Last in the UK?

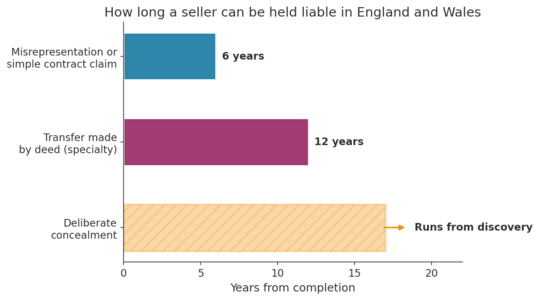

Seller liability in the UK is shaped by the Limitation Act 1980, which sets the clock on most property claims. For a standard breach of contract or a misrepresentation, a buyer has six years from completion to issue proceedings under section 5 of that Act.

Where the property was transferred by a deed, the window can stretch to twelve years. Section 32 then pauses the clock for fraud or deliberate concealment, so the count only begins once the buyer discovers, or reasonably should have discovered, the problem.

Statutory time limits for seller claims. The concealment bar is illustrative: the clock starts when the buyer discovers the issue.

| Worth remembering: the sooner after a sale a claim surfaces, the easier it is for a buyer to prove the fault was already present, which strengthens their case. |

A 2025 High Court ruling shows how far this can reach. In Patarkatsishvili and Hunyak v Woodward-Fisher, buyers of a £32.5 million Notting Hill mansion were allowed to unwind their 2019 purchase after the seller failed to disclose a serious moth infestation.

Long after completion, a court can still order the contract reversed and the purchase price repaid.

The Three Legal Grounds That Create Seller Liability

Three legal grounds account for almost every claim brought against a former owner: misrepresentation, misdescription, and defects in the home itself. The table below sets out what each one means.

| Legal ground | What it means | Typical example |

| Misrepresentation | A false or misleading statement that persuades the buyer to proceed. | Saying the home has never flooded when it has. |

| Misdescription | Inaccurate details about the property itself. | Overstating plot size or claiming a boundary you do not own. |

| Defects | A fault that existed during your ownership and was known to you. | Concealed subsidence, faulty wiring, or active damp. |

Misrepresentation

Misrepresentation occurs when you give false or misleading information that encourages a purchase. It can be fraudulent, where you knew the statement was false, negligent, where you made it without checking, or innocent, where you believed it but were mistaken. Even an honest slip can find a claim under the Misrepresentation Act 1967, because what matters is whether the buyer relied on your words.

| Type | Definition | Usual outcome |

| Fraudulent | You knowingly gave false information. | Damages, and the sale can be rescinded. |

| Negligent | You made a statement without reasonable grounds. | Damages, and possible rescission. |

| Innocent | You honestly believed an inaccurate statement. | Damages in lieu, or rescission in some cases. |

Misdescription

Misdescription covers wrong information about the property’s physical facts, such as its dimensions, characteristics, or the rights attached to it. Overstating a garden’s size or asserting a right of way that does not exist can both leave you exposed to a claim.

Defects in the Property

Property defects fall into rough bands. Structural faults affect the walls, roof, or foundations and can make a home unsafe. Functional faults involve systems such as wiring or plumbing. Cosmetic issues are minor, though they still count if you actively concealed them. A defect only weighs against you when it was present while you owned the home and you knew of it.

The TA6 Form and Why Your Answers Matter

The TA6 Property Information Form, produced by the Law Society, is the standard disclosure document completed by the seller during the conveyancing process to tell the buyer about the home. Your answers become part of the contract of sale, so accuracy carries real weight.

The paperwork has been refreshed. The sixth edition replaced the older versions on 30 March 2026 and uses clearer “are you aware” wording, letting you reply “not known” where you genuinely cannot say. You can view the current document through the Law Society’s updated disclosure form.

| ⚠ Watch out: a vague or partly true answer can be treated as a misrepresentation, even when it is technically accurate. Significant building work carried out before the property was yours still needs declaring. |

Regulation around disclosure has tightened too. The Digital Markets, Competition and Consumers Act 2024, in force from April 2025, replaced the old Consumer Protection Regulations for unfair commercial practices and is now enforced by the Competition and Markets Authority.

How Sellers Are Protected From Liability

Sellers are not left fully exposed, because the law also expects buyers to do their own homework before committing.

Caveat Emptor and Buyer Surveys

Caveat emptor, meaning let the buyer beware, places a duty on purchasers to investigate before they commit. A buyer who skips a proper survey may struggle to claim afterwards for a fault that an inspection should have caught. Pointing them towards the right survey for an older property, and checking your grounds before you sell, works in everyone’s favour.

Contract Disclaimers

A disclaimer clause adds another layer of cover. If your buyer learns of a defect and still wishes to go ahead, your solicitor can record in the contract that they bought with full knowledge of it.

Indemnity Insurance

Indemnity insurance guards against specific risks, often missing certificates or guarantees for past work. It is a sensible safety net, yet it will not rescue anyone who deliberately misled a buyer, since dishonesty voids the cover.

How to Reduce Your Liability When Selling

Lowering your risk comes down to honesty, paperwork, and good advice. The actions below do most of the heavy lifting.

| What to do | How it protects you |

| Disclose known faults early | Takes away the main grounds for a later claim against you. |

| Complete the TA6 form fully and truthfully | Stops a wrong or vague answer becoming a contractual breach. |

| Keep certificates, guarantees, and repair quotes | Provides evidence that work was done and described accurately. |

| Instruct an experienced conveyancer | Helps you answer enquiries correctly and spot risks in advance. |

| Consider indemnity insurance for paperwork gaps | Covers defined risks such as a missing building certificate. |

Owning up to a fault may invite a lower offer, but that cost is tiny next to a court claim and the worry it brings. Gather repair quotes so you can negotiate from a position of knowledge.

Professional handling makes all of this easier. In a Google review, Francesca Stafford praised the team at Oliver Jaques for guiding her house sale from the start and managing viewings smoothly, the kind of organised, transparent approach that keeps disputes at bay.

Frequently Asked Questions

Can a buyer take you to court after completion?

Yes. A buyer can sue a former owner for misrepresentation or breach of contract after completion, usually within six years. They must show the fault existed beforehand and that they relied on inaccurate information you supplied during the sale.

How long after selling can a buyer claim for a hidden defect?

Most claims must be issued within six years of completion under the Limitation Act 1980. Where you deliberately concealed the defect, that period can start from the date the buyer discovers it, extending your exposure considerably.

Do you have to disclose everything when selling a house?

You are not obliged to volunteer every detail, but you must answer the TA6 and any enquiries honestly. Giving false or misleading replies is what creates liability, rather than staying silent on matters nobody asked about.

Does indemnity insurance cover misrepresentation?

No. Indemnity policies cover named risks like missing building certificates, not deliberate dishonesty. If you knowingly misrepresent the property, the insurer can refuse to pay and you remain personally liable for any successful claim.

What happens if you accidentally got an answer wrong?

An honest mistake can still support an innocent misrepresentation claim if the purchaser leaned on it and suffered a loss. Tell your solicitor the moment you spot an error so the record can be corrected before completion.

Final Thoughts

Selling up rarely ends every responsibility on the day you complete. For about six years afterwards, and longer where concealment is involved, the answers you gave can still return to haunt you. The fix is refreshingly simple: fill in the TA6 form honestly, keep your certificates and quotes, lean on a capable conveyancer, and weigh up indemnity cover for gaps in your records. Treat openness as the cheapest insurance you own, and a smooth sale today stays a settled one tomorrow.

References

Law Society, TA6 Property Information Form (6th edition), 2025 — https://www.lawsociety.org.uk/topics/property/ta6-6th-edition

Legislation.gov.uk, Misrepresentation Act 1967 — https://www.legislation.gov.uk/ukpga/1967/7/contents

Legislation.gov.uk, Limitation Act 1980 — https://www.legislation.gov.uk/ukpga/1980/58/contents

England and Wales High Court, Patarkatsishvili and Hunyak v Woodward-Fisher [2025] EWHC 265 (Ch), 2025 — https://www.bailii.org/ew/cases/EWHC/Ch/2025/265.html

Legislation.gov.uk, Digital Markets, Competition and Consumers Act 2024 — https://www.legislation.gov.uk/ukpga/2024/13/contents

Fact Check: All statistics and data points in this article were verified against original sources as of 12 June 2026. Sources are listed in the References section.

Ref : 4337.37926

POSTED BY

POSTED BY