Meta Title: Meta Description: UK investors can own freehold homes in Dubai with no local property, income or capital gains tax, roughly 4% in transfer fees and gross yields near 7%.

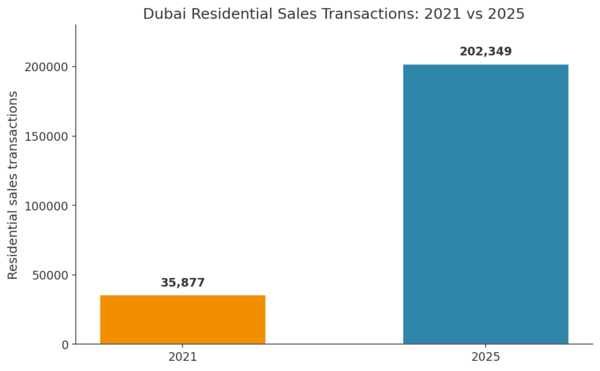

British buyers are looking further afield for stronger returns, and one city keeps topping the shortlist. Dubai recorded more than 202,000 residential sales in 2025, a record year that drew fresh money from across the United Kingdom.

The pull is easy to understand. There is no local charge on rental income or capital gains, gross yields sit well above most British cities, and the purchase journey is fast and largely digital.

The rules do differ from a domestic deal, though, and small slips can prove expensive. This guide sets out what UK buyers should know, from freehold zones and fees to financing, residency and the tax you still owe back home.

Key Takeaways

- British nationals can own freehold homes outright in designated Dubai zones, with no residency needed to purchase.

- The emirate levies no local tax on rental income, capital gains or annual ownership.

- Set aside roughly 7 to 10 percent above the price for fees and registration.

- Gross yields reached about 7 percent for apartments and 5 percent for villas in 2025.

- UK tax residents must still declare foreign rental earnings to HMRC.

Can UK Citizens Buy Property in Dubai?

Yes. British citizens may purchase freehold homes in the emirate without holding residency or a visa. Foreign ownership is allowed within designated freehold zones, where you hold the home and the land outright, with the right to sell, let or pass it on.

Intra Capital Estates explains how to buy a house in Dubai from first enquiry through to title transfer, which is worth a read before you start.

Freehold areas cover many of the most sought after communities, among them Dubai Marina, Downtown, Palm Jumeirah, Business Bay, Jumeirah Lakes Towers and Dubai Hills Estate. Beyond these zones you may only take a long leasehold, often spanning 90 or 99 years.

|

Pro tip: confirm a home sits inside a freehold zone before you part with any money. An agent who works with British clients can verify this in minutes. |

Why Dubai Appeals to UK Property Investors

Dubai gives British investors a blend that few mature markets can match: light taxation, high yields and a swelling tenant pool. The emirate passed 4 million residents in 2025, and that growth keeps rental demand firm across the most popular districts.

Record transaction volumes show how quickly demand has built. The figure below puts the scale of recent growth in context.

Tax Efficiency and What You Still Owe

The UAE applies no annual property tax, no capital gains tax on a sale, and no charge on collected rent. That structure leaves more of every payment in your pocket, which is the headline draw for income focused buyers.

There is a catch many overlook. If you remain a UK tax resident, you are taxed on worldwide income and must report that rental money to HMRC, even when the cash never reaches a British account. Gains on a future sale can also fall within UK rules.

Compared with other global hotspots such as investing in New York property, the emirate stands apart for leaving local rent untaxed while you build equity.

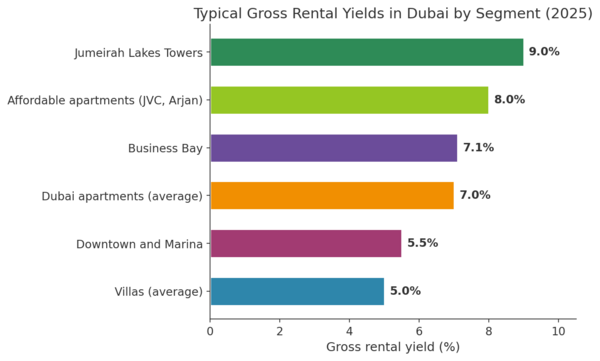

Rental Yields and Tenant Demand

Gross rental yields in Dubai averaged near 7 percent on apartments, with villas closer to 5 percent, measured at the close of 2025. Returns vary sharply by district, with affordable communities tending to outperform prime addresses on income.

Affordable communities such as Jumeirah Lakes Towers delivered gross yields close to 9 percent in 2025, well above the typical 5 to 6 percent seen across UK cities.

Smaller, well located flats often deliver the strongest figures, while waterfront villas trade some yield for capital growth. The chart below shows how returns differ across the market.

Dubai also ranks among the cities with the highest property returns worldwide, which is why portfolio diversification draws so many overseas buyers.

Here is how the emirate stacks up against a typical UK investment purchase.

|

Factor |

Dubai |

United Kingdom |

|

Annual property tax |

None |

Council tax applies |

|

Capital gains tax (local) |

None |

Applies on residential gains |

|

Tax on rental income (local) |

None |

Income tax applies |

|

Purchase or transfer cost |

About 4% transfer fee |

Stamp duty, plus buyer surcharges |

|

Typical gross yield |

Around 5% to 9% |

Around 5% to 6% |

|

Residency through purchase |

From AED 750,000 |

Not linked to a purchase |

What It Costs to Buy in Dubai

Purchase costs in the emirate sit below UK stamp duty, yet they still mount up and deserve careful budgeting. The largest single item is the Land Department transfer fee, set at 4 percent of the price.

Most deals are registered through the Dubai Land Department or one of its trustee offices, which keeps the official record of who owns what. On top of that levy you should plan for agency commission, a registration charge and, if you borrow, a mortgage fee.

|

Cost |

Typical amount |

|

Land Department transfer fee |

4% of the property price |

|

Agency commission |

Around 2% of the price |

|

Registration (trustee) fee |

AED 4,000 plus VAT (price AED 500,000+) |

|

Title deed issuance |

Around AED 580 |

|

Mortgage registration (if financing) |

0.25% of the loan plus AED 290 |

|

Total upfront extras |

Around 7% to 10% of the price |

|

Budget check: on a home priced at AED 2 million, upfront costs of 7 to 10 percent mean roughly AED 140,000 to AED 200,000 on top of the purchase price. |

How the Buying Process Works

The Dubai purchase journey is quicker than a typical British sale and runs mostly online, although the order of steps will feel new. For a ready home, the path looks like this:

- Set your budget and gather proof of funds or arrange a mortgage in principle.

- Pick a RERA licensed broker or deal directly with the developer.

- Agree terms and sign the Memorandum of Understanding, known as Form F, paying a deposit of around 10 percent.

- Obtain the developer No Objection Certificate, which confirms no service charges are outstanding.

- Transfer the title deed at a registration trustee office, taking your passport along.

Cash buyers can often wrap up in two to four weeks where a home is ready to sell. Adding a mortgage stretches the timeline by roughly a fortnight.

Ready Homes Versus Off-Plan

A completed home lets you rent it out at once, giving instant income and a property you can inspect in person. An off-plan purchase, bought before construction finishes, usually carries a lower entry price and staged payments into a protected escrow account, with stronger potential upside on completion.

The trade off is timing risk, since handovers can slip. Off-plan stock made up roughly 63 percent of 2025 sales, so it clearly suits plenty of buyers. Unlike the conveyancing process back home, much of the Dubai paperwork is handled through government apps.

Video: “How UK Investors Buy Property in Dubai?” — https://www.youtube.com/watch?v=0r7_PTd23lU

This short video walks through how British buyers approach a Dubai purchase and what to weigh up first.

What Buyers Say About Working With an Agent

Jonathan, a buyer who left feedback on the Intra Capital Estates testimonials page, described being well supported at every stage, with clear communication and problems solved in a resourceful way. His account reflects the value of guidance when a cross border purchase has more moving parts than a local one.

Can You Gain Residency by Buying in Dubai?

Property ownership in the emirate can unlock long term residency, which is a genuine bonus alongside the income. An investment of at least AED 750,000 can qualify you for a two year investor visa.

Step up to a certified value of AED 2 million or more, and you become eligible for the ten year Golden Visa, which is renewable and lets you sponsor close family. The current market value, not the original purchase price, decides eligibility.

|

Key figures: AED 750,000 unlocks a two year investor visa; AED 2 million in certified value qualifies for the renewable ten year Golden Visa. |

What UK Investors Should Watch Out For

The dirham is pegged to the US dollar, so the sterling cost of a deal shifts with the GBP to USD rate. Moving funds at a sensible moment can save thousands on a larger purchase.

A few other points deserve attention before you commit:

- Off-plan handovers can run late, so stick to developers registered with RERA and read the payment schedule closely.

- Service charges apply to apartments and managed communities, often quoted per square foot each year.

- Your HMRC duties continue, so keep records of rent and expenses for self assessment.

Looking at where British buyers are purchasing abroad shows Dubai competing hard with traditional European favourites on both lifestyle and return.

|

Warning: never transfer a deposit until you have confirmed the seller, the property registration and the trustee office details in writing. Large cross border payments are a target for fraud. |

Frequently Asked Questions

Can a non resident purchase a Dubai home?

Yes. Non residents may buy freehold property in designated zones without a visa or UAE residency. You can pay in cash or apply for an international mortgage if you meet a lender criteria, and the whole process can be handled remotely.

Do British buyers pay tax on a Dubai home?

Locally, no. The UAE applies nothing on the rent you collect, on gains or on what you hold. However, if you are UK resident for tax, you must report the rental income to HMRC and could face UK capital gains when you sell.

How much deposit do non residents need for a mortgage?

Most UAE lenders ask non residents for a deposit of at least 20 to 25 percent, sometimes more. A pre approval before you view homes clarifies your budget and strengthens your hand when negotiating.

How long does it take to complete a purchase?

A cash buyer can complete within about a month when the home is ready. Financing adds roughly two weeks for the mortgage, while an off-plan unit depends on the build schedule and any snagging.

Is buying off-plan in Dubai safe?

It can be, with care. Developer instalments go into a regulated escrow account, which protects your money, and choosing a RERA registered developer lowers the risk. Always check the contract terms and the firm track record first.

Conclusion

Dubai rewards British buyers who do their homework: a tax light setting, strong yields and a quick, transparent process that opens the door to residency. The market moves fast, so clear budgeting and a trusted local agent matter more than chasing the lowest headline price. Treat the purchase as you would any serious investment, line up your funding and tax position early, and the emirate can sit comfortably at the heart of a diversified portfolio for years to come.

References

Engel & Völkers, Dubai Housing Market 2026, January 2026 — https://www.engelvoelkers.com/ae/en/resources/dubai-housing-market

Dubai Land Department, Property Sale Registration, 2026 — https://dubailand.gov.ae/en/eservices/property-sale-registration/

GOV.UK, Tax on Foreign Income, 2026 — https://www.gov.uk/tax-foreign-income

Global Property Guide, UAE Residential Property Market Analysis 2026 — https://www.globalpropertyguide.com/middle-east/united-arab-emirates/price-history

Property Finder, DLD Fees Dubai Complete Costs Guide, 2026 — https://www.propertyfinder.ae/blog/dld-fees-dubai/

Fact Check: All statistics and data points in this article were verified against original sources as of 10 June 2026. Sources are listed in the References section.

POSTED BY

POSTED BY